Personal AI digital twins: the future of human interaction?

AI takes jobs, AI creates jobs, AI accelerates the pace of change all around you. How will…

"FinTech innovation: A Balancing Act Between Disruption and Regulation” is the title of the latest EIT Digital Makers & Shapers report presented today at an invitation-only event in Brussels. The report provides an in-depth analysis of the growth and evolution of the FinTech industry in Europe over the past five years, and the challenges regulators face in fostering innovation while managing emerging risks.

The latest thought leadership report highlights several key drivers spurring the rise of FinTech startups and digital financial services. These include rapid advances in technologies like blockchain, artificial intelligence and open data platforms. Another factor is changing consumer preferences, especially among younger demographics, for more convenient, personalised and mobile-based financial services.

There is also growing demand for greater efficiency and transparency in financial transactions. Legacy processes at incumbent banks are often cumbersome and opaque. FinTech innovations like automated investing platforms and digital wallets offer streamlined digital experiences.

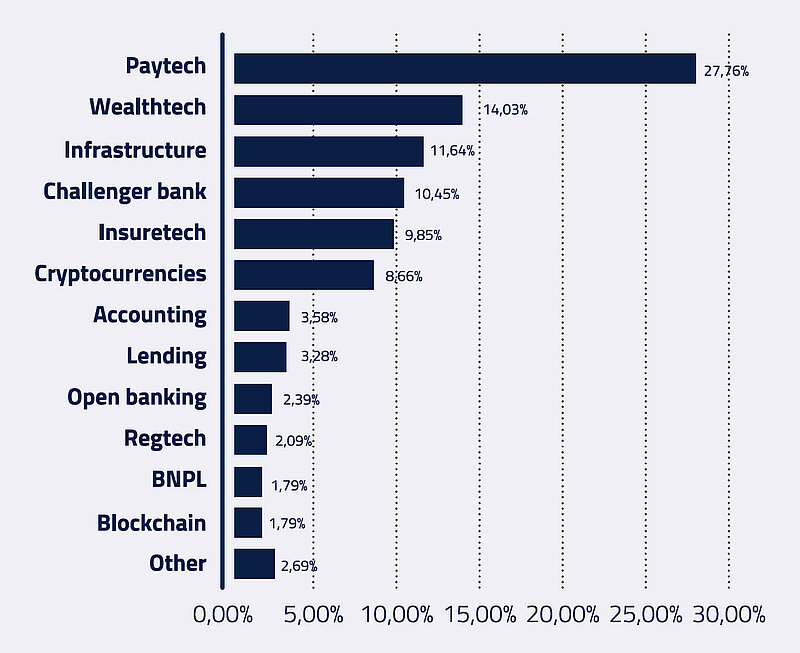

These drivers of change have opened opportunities for agile startups to gain footing by focusing on niches overlooked by established institutions. The report notes FinTech growth has been particularly marked in the payments sector, with 93 of the top 335 FinTech "unicorns" globally providing various payment solutions.

While initially seen as disruptive, collaboration between FinTechs and incumbent banks is increasing. Each side brings complementary strengths. Startups offer innovative technologies and business models, while banks provide regulatory expertise, funding and extensive customer bases.

However, FinTechs still pose competitive threats to traditional banking, especially in areas like payments, lending, and personal finance management. Their lower operational costs and increased use of data for personalization allow them to provide better user experiences at lower fees.

The report emphasizes that regulators across Europe have struggled to keep up with the rapid emergence of new markets, products and risks created by FinTech. Many startups have benefited from "light touch" oversight in their early stages.

But as the industry matures, regulators are taking a more active role in balancing encouraging further innovation with managing risks around consumer protection, fair competition, and financial stability.

For example, the explosion of cryptocurrencies like Bitcoin led to extreme volatility and huge losses for some retail investors. In response, the EU introduced new regulations like the Markets in Crypto-Assets (MiCA) framework to establish clearer oversight.

Areas of concern highlighted in the report include potential over-indebtedness from new digital lending platforms. There are also growing risks from services reliant on harvesting and exploiting consumer data.

The report notes EU policymakers aim to facilitate FinTech innovation by providing regulatory clarity, open banking rules to spur competition, and fostering collaboration through innovation hubs.

But finding the right balance remains an ongoing challenge. The report advocates for proportionate regulation tailored to specific activities and risks, rather than restrictive one-size-fits-all rules. It also calls for restrictions on higher risk offerings to retail consumers, like crypto assets.

In its conclusions, the report underscores the need for regulators to continue enhancing their technological expertise and agility to keep pace with the rapid digital transformation of finance.

It also identifies 4 key scenarios for how regulation and market dynamics could shape the future evolution of the FinTech industry across Europe.

Overall, our Makers & Shapers report "FinTech innovation. A balancing act between disruption and regulation" provides valuable insights into the profound changes underway in European finance thanks to FinTech innovation. It highlights the delicate balancing act required to manage risks while safeguarding consumer welfare and market stability.

At the same time, it identifies targeted actions that can create an enabling environment where startups and incumbents alike can leverage technology to expand consumer choice, efficiency and competitiveness. EIT Digital invites stakeholders across the financial services ecosystem to engage with us as we keep exploring these crucial issues through practical education, research and entrepreneurship programmes. Let’s continue the conversation and join forces to shape the future of digital finance in Europe!

Receive the latest news and events updates by subscribing to our newsletter.

Are you a member of the media and would you like to contact us?

→ Get in touch with us here

May 14, 2024

May 14, 2024

AI takes jobs, AI creates jobs, AI accelerates the pace of change all around you. How will…

April 29, 2024

April 29, 2024

In the vibrant landscape of Italian startups, an emerging player is gaining attention for…

April 18, 2024

April 18, 2024

At the prestigious Delphi Economic Forum in Greece, EIT Digital took center stage to…

April 17, 2024

April 17, 2024

EIT Digital is delighted to welcome Riga Technical University (RTU) as a valued addition…

April 16, 2024

April 16, 2024

Have you ever found yourself in a doctor's office, asked to take three deep breaths, and…

April 8, 2024

April 8, 2024

Navigating the world can be a daunting challenge for individuals with visual impairments,…

Co-Funded by the European Union